Saxco Update - July 2025

Tariff relief offers short-term breather; long-term uncertainty remains

Welcome to July’s update from our friends at Saxco, on market dynamics in beverage packaging.

This update first appeared as a paid subscriber feature in the Ciatti California Report on July 10. If you are not yet a paid subscriber and would like full access to the monthly California Report, its actionable bulk wine and grape market intelligence, bulk inventory charts by volume and by varietal, and bulk/grape market activity barometer, you can check out our subscription plans by clicking this button.

Packaging supply stable, but uneasy

While June ushered in a more stable rhythm after May’s tariff-driven frenzy, underlying uncertainty continues to shape planning, procurement, and pricing across the packaging and logistics landscape.

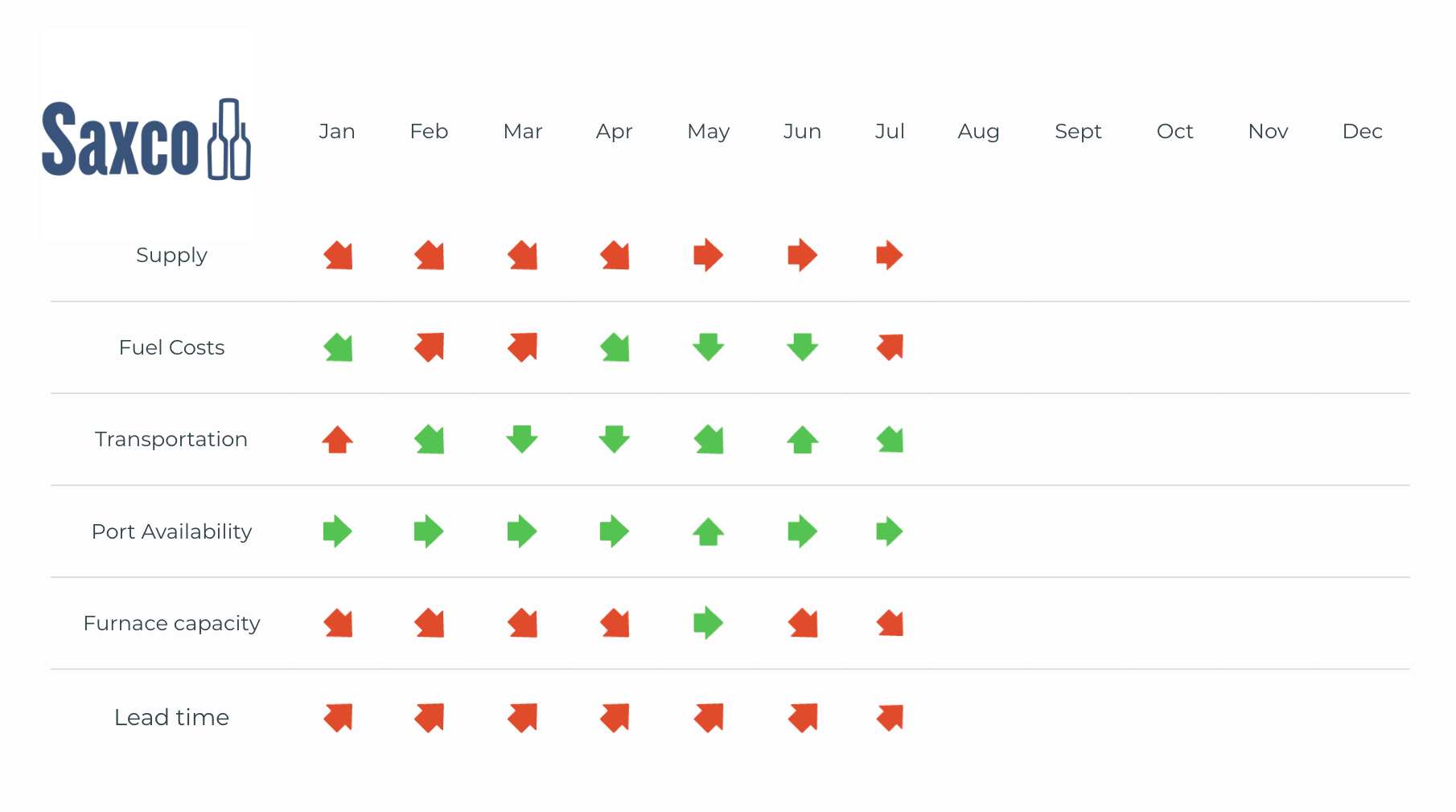

Supply remains steady across most categories, but stability doesn’t mean simplicity. US glass manufacturers, in particular, are contending with a mismatch between output and demand. Inventories have piled up amid sluggish ordering, especially from wine producers still reeling from compressed consumer spending and slowing DTC velocity. With tanks and warehouses more full than empty, some domestic furnaces are now eyeing Q3/Q4 production pauses as a measure to rebalance.

After a brief reprieve in May, diesel prices rose again in June, increasing from $3.499 to $3.599 per gallon, a continued reflection of the volatile energy market. According to the latest Deloitte economic outlook, while core inflation is showing signs of moderation, energy prices remain sensitive to global geopolitical tension and supply disruptions – factors that could ripple into transport costs if sustained.

A welcome shift: Ocean freight rates are finally softening. The temporary spike in May – triggered mainly by the rush to export from China after the Trump administration’s tariff adjustment announcement – has now normalized. With much of that panic-driven demand behind us and Peak Season Surcharges dropping off for July, space is opening up and rate pressure is easing. Expect less turbulence and better booking windows through mid-summer, especially for trans-Pacific lanes.

No major disruptions at key US ports this month. Container flow has steadied, and with fewer surcharges in play and less congestion at origin points in Asia, downstream bottlenecks are easing. However, West Coast labor agreements and geopolitical flashpoints remain lurking variables to monitor.

Domestic furnace capacity remains technically stable, but looming stress is on the horizon. As noted, with US manufacturers holding higher-than-normal inventory and facing muted forward demand, the sector may reduce operating throughput later this year. Manufacturer inventory recalibrations could impact availability and price negotiations for Q1 2026, especially for custom molds or specialty projects.

Lead times remain elevated across glass and closures, with no significant change from May. Extended replenishment cycles are being driven by a combination of slower burn rates, cautious forward ordering, and lingering backlog from earlier transportation disruptions.

While last month’s flurry stemmed from the announcement of lower tariffs on Chinese glass, that has since cooled, but uncertainty remains. The tariffs remain in place, and the administration has signaled that the policy could shift again in the future. Wineries should continue to hedge with a balance of domestic and international sourcing, and closely monitor the ever-changing tariff policies.

According to Deloitte’s June 2025 economic forecast, the broader US economy continues its “soft landing” trajectory – growth without recession, but not without friction. Consumer sentiment has improved slightly, but spending remains cautious, particularly in categories tied to discretionary lifestyle purchases (like wine). For suppliers, this means maintaining agility and avoiding overextension.

The worst of the tariff-related chaos may be behind us, but we are not yet in calm waters. Pricing, transportation, and inventory planning all require careful attention through the remainder of summer.

Bottled Tidbits - The origin of the ‘punt’ in a bottle remains a topic of debate. Some say it was used to collect sediment in the days before wine filtration became a common practice. Others argue it helped glassblowers shape the bottle or added strength for sparkling wines under pressure. There’s even speculation that punts made bottles easier to stack – or made pouring feel more ceremonial. But in reality, punts originated from the practical needs from the days when bottles were only glass-blown. When bottles were hand-formed, the base seam was pushed inward to ensure the bottle could stand upright and to eliminate the sharp glass tip that formed during the blowing process – a simple solution that became a lasting design feature.

Today, the punt persists primarily as a tradition and marketing tool. A deeper punt still often signals a more “premium” bottle. The practical need evolved from form to folklore until the punt became a visual shorthand for luxury and now has become a packaging cue, subtly signaling quality and prestige, regardless of what’s actually inside the bottle.