Ciatti California Report - August 2024

Heatwave arrives; grape market remains slow

July was likely the warmest on record for much of the western US, with California receiving the highest heat levels and areas of the Central Valley suffering two weeks of 100-110°F temperatures. The heat has since dissipated slightly in early August, although consistent, more normal temperatures in excess of 85°F are forecast. The general feeling is that vineyards across the state will have been affected by such a prolonged heatwave: Some – limited – burn damage has been in evidence and there is a suspicion that berry sizing has been hindered.

The dividends from California’s wet winter are now making themselves felt: Despite the hot summer, soil moisture levels in many places remain relatively good – even at this stage – and canopies appear healthy. Given this and the fact many cash-strapped growers are economizing on treatments, there has been some mildew pressure, but still at normal levels. Also normal is timing, with ripening proceeding perhaps 2-4 weeks ahead of last year’s greatly-delayed season: Harvesting of some early-season whites got underway in the Central Valley during the last week of July and is expected to commence in some Coastal areas in mid-August.

Picking of the whites in the Valley so far has revealed a lightness, but it remains too early to draw firm conclusions or extrapolate out an overall crop size. Given the slowness of the grape market heading into the growing season, and then the climactic factors of the past month, the present suspicion is that the crop could be average-sized at best. By area, the crop potential currently appears average-sized in the North Coast, lessening in size in the Central Coast from north to south, and below average in the Interior. Continued intense heat could potentially lead to a tightening of crush capacity and storage supply if everything ripens all at once.

After a milder 2023, wildfires have unfortunately returned as a backdrop to the Californian summer. Some wineries have been carrying out spot testing of grapes for smoke exposure; no issues have been reported as yet and we do not anticipate smoke becoming a problem. Testing may simply be part of a stricter enforcement, by wineries, of quality standards set out in contracts with grape suppliers, in a time when grape need is limited. Contracted growers have been receiving letters from their wineries stating that contract maximums will be adhered to this year and that grapes failing to meet quality standards risk being rejected.

It continues to be a highly challenging time for many growers. Those with vineyards uncontracted – some of them perhaps uncontracted for a second consecutive year – will need to decide what to do with their grapes. Custom crushing is high risk, given the ongoing slowness of the bulk market. We therefore expect to see fruit left on the vine, like last year, which makes predicting a crop size all the more challenging.

This is the first month in which the entirety of the Ciatti California Report is on Substack. To read the report, simply keep reading below, clicking on images to enlarge them.

For the most up-to-the-minute information, get in touch with Ciatti directly. The broker team includes industry professionals with over 135 years of collective experience, ready to help buyers and sellers alike navigate through this challenging period and beyond. For Ciatti head office and individual brokers’ contact details, hit this button.

The Grape Market

The grape market’s continued slowness into August, with harvest 2024 just starting to get underway, is a significant concern. Much of the limited activity that has occurred has been re-signs from last year, mostly for very limited tonnages.

Demand for Napa Cabernet grapes is surprisingly quiet, so too inquiries into other cachet items such as Russian River Pinot Noir and Russian River Chardonnay. The market for these feels almost as depressed as for other grapes. It may be that potential buyers are biding their time until later during harvest, by which time prices may have reduced further.

White varieties lead interest

Whites lead interest on the grape market, in both the Coast and the Interior; for example, we have seen some activity on Coastal Chardonnay and Sauvignon Blanc. The short-term reason for white grape interest noticeably leading red may be suspicions – stimulated by the aforementioned early picking results – of a shorter crop on these varietals (or at least less chance of there being overage opportunities). Longer term, white wines seem to be in slightly healthier consumer demand than reds, with recent Nielsen IQ data showing whites had increased their share of the total table wine market in the US from 48.5% to 49.2% in the 52 weeks ending May 18th, and to 50.5% in the four weeks to that date. This has been attributed to growing consumer preference for lighter wines as well as wine-based cocktails.

That said, Chardonnay’s bulk wine inventory remains larger than it was a year ago. Indeed, the ongoing bulk wine availability on all varieties acts as a significant disincentive for buyers to move onto the grape market at a time when the overriding sentiment around supply is: If in doubt, go without. Many wineries that purchased 2023 grapes on the spot market did not subsequently see the expected upside, leading to continued caution this year. A spot market for 2024 grapes could still develop, but it is currently hard to imagine who the buyers would be and at what price they would come onto the market.

Therefore, we encourage grape suppliers to cast a wide net for potential buyers and to be open to offers. The best way of doing this is to have grapes listed with us at Ciatti and as early as possible, as it assists us in finding a buyer when activity does arise. Growers should keep us up to date with the 2024 grapes they may have for sale by contacting Molly at +1 415 630 2416 or molly@ciatti.com. Potential buyers of grapes trying to get a feel for what is available are also welcome to reach out to us.

Finding buyers via Ciatti also helps grape suppliers avoid inexperienced interested parties who may be opportunistically entering the market without necessarily having the financing or infrastructure to support their ambitions. The market is currently a highly challenging one to navigate for even the most experienced wine industry professional, let alone the inexperienced new entrant. Grape suppliers must be careful to ensure they do not pick their grapes on the understanding of a contract – and money – that does not then materialize.

To custom crush or not to custom crush?

We also reiterate our caution regarding custom crushing. Hope is not a strategy: Custom crushing should only be embarked upon as a serious, strategic business diversification that takes into account the attendant costs and the ongoing slowness of the bulk market. Many growers who custom-crushed in 2023 are unlikely to do so again given the ensuing difficulty in moving their wines and – indeed – some wineries have signalled they are, as a rule, unlikely to carry out custom crushing for growers this year as they see it as a risk to themselves in terms of tank space.

Vine removals continue across the state and will continue if market conditions do not improve, with growers removing older vines and non-prime sites in order to cut their losses. Some 40,000 acres are believed to have already been removed – we appreciate the work Allied Grape Growers are doing to keep the industry updated on this.

Wineries and vineyards continue to be put up for sale. This is a consequence of the present difficulties around profitability in the wine industry, of course, but also other factors, such as generational change – as owners from the baby-boomer generation retire – and the fragility of the wider economy. From our discussions with major agricultural real estate brokers, we know there is limited buyer interest at current prices. Asset prices getting significantly discounted in order to help attract buyers can, in turn, downwardly valuate the assets and borrowing power of the wider industry.

On July 24th, Vintage Wine Estates (VWE) announced it was filing for Chapter 11 bankruptcy, which allows it to “address outstanding debt obligations while the business pursues the sale of its assets”. VWE said it had “experienced negative financial headwinds that severely impacted its liquidity position”. This situation will potentially adversely affect some of VWE’s creditors and financing structures, adding further strain on the overall market. The sale of VWE assets could – as mentioned above – soften the value of assets elsewhere in the industry, in turn reducing borrowing power.

The Bulk Market

A stabilization in wine sales at US retail – or at least a return to stable demand from retailers and distributors – is yet to manifest itself. If ‘flat’ is the new ‘up’ in terms of sales, we have not seen the new ‘up’ yet and the sunnier forecasts of earlier in the year have still to be born out.

In the summer 2024 edition of their Wine Market Observations and M&A Review, business management consultants Azur Associates issued a more neutral outlook, stating that while “there are more wine consumers than 10 years ago” and that supply overages have led to lower prices and, in turn, given consumers “high quality wines that over deliver”, consumers remain economically-challenged, are consuming less wine and “spreading consumption occasions across beverage alcohol”, a repertoire “as wide as it’s ever been”. It asked the tough question: “Are there too many wineries in the US?” – their numbers having risen from less than 5,000 in 2004 to in excess of 11,000 in 2020 – and said that, in 2023, the long-term growth in winery numbers had started to reverse. Dovetailing with our comment above in the Grape Market section, Azur stated that current winery M&A activity reflects “a cautious macro environment and an ‘oversupply’ of wineries who would like an exit”.

Bulk market activity through July remained at the better levels seen in May and June versus preceding months, albeit still sluggish from a historical perspective. Buying has likely been encouraged by softened pricing – suppliers are increasingly willing to sell at lower prices in order to empty tank space pre-harvest – and some buyers opting for bulk wine ahead of grapes, at the expense of the grape market.

Inventory remains considerable: Our bulk inventory chart for August shows that Chardonnay supply has reduced every month since May, but Cabernet now totals well beyond 10 million gallons and Pinot Noir and Zinfandel stocks are also large. Overall bulk inventory this August is well above August 2023 levels. Some California-appellation inventory is moving at $1-2/gallon which, while not ideal for individual suppliers, helps relieve this burden of oversupply. These low prices are at one end of a downward cascade in pricing, from the Coast into the Interior, which opens up opportunities across the state for buyers to harness deals providing an unmatched price-quality ratio: We have not before seen the buying opportunities the like of which we are seeing now.

What wines have led interest?

Wines that have led interest over the past couple of months have included 2023 generic reds or red blenders (at least for a short time), 2022 and 2023 Napa Cabernet (although interest levels have been lower than historically, as on grapes), 2022 and 2023 Cabernet from various areas including the Coast, and 2023 Coastal Chardonnay. Any transactions that do result from this interest are often characterized by the buyer finding wines of the quality they seek at exactly the pricing they seek – there is little if any room for suppliers to negotiate on price. More transactions would potentially occur if the price-quality ratio of the wines being offered better corresponded to buyer expectations: Sometimes the price may be right for the buyer but the quality not, while the quality they desire is still at a price they are unwilling to pay.

The approach of suppliers is not uniform: Some have been happy to compromise significantly on price in order to move wines on, while others remain more bullish, perhaps holding out for the large-volume deal that might empty their tanks at a stroke instead of selling piecemeal, even if the latter may involve a higher price. Some have been slow to respond to sample requests. Sending their samples in to us remains the best way for bulk wine suppliers to find a buyer. Suppliers can contact either Mark at +1 415 630 2548 / mark@ciatti.com or Michael at +1 415 630 2541 / michael@ciatti.com to get their wines listed. Buyers requiring wine should get in touch so we can send samples their way.

Who are the prospective buyers?

Many of the prospective buyers at the moment seem to be those seeking to fulfil private label programs or put specific blends together for which they perceive there is a gap in the market. Some are seeking multi-year supply; most are seeking low prices.

How active buyers will be in the coming weeks remains to be seen: Will activity dissipate as the industry focuses squarely on harvest, or will it be spurred on if the crop looks like coming in shorter than the average? Looking further ahead, and being more hopeful: If wineries have moved themselves back into balance after taking in only those 2023 grapes they had contracted, and an even smaller number of 2024 grapes (having let some contracts lapse between vintages), could their need for bulk wine rise rapidly if or when retailer/distributor demand returns?

By fall, 2023 wines will continue to possess value but older vintages will struggle, especially the whites. Volumes of 2022 white varietals still remain and will struggle to be sold as anything other than generic wine at generic-wine prices. Demand from the grape juice concentrate industry currently remains negligible; GJC players agilely managed their 2023 production and appear to be in balance.

For Ciatti head office and individual brokers’ contact details, hit this button.

Saxco Update

Welcome to August’s update from Saxco on market dynamics in packaging.

Despite the macro-economic challenges, the CrowdStrike outage, the geopolitical tensions, and the exciting Olympics, the wine packaging market has remained rather stable for the last month.

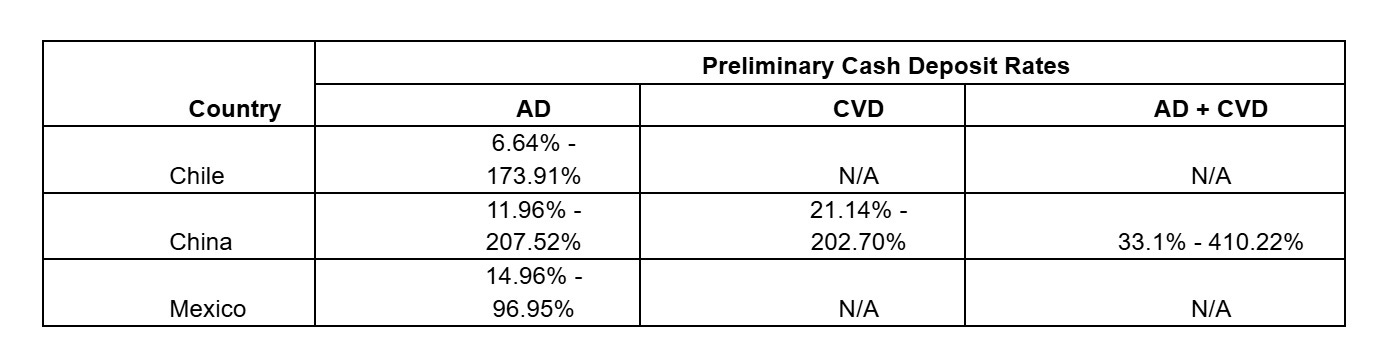

However, the US Department of Commerce (Commerce) recently made affirmative preliminary antidumping (AD) determinations regarding glass wine bottles and similar glass bottles (740ml-760ml) imported from China, Mexico, and Chile.

As a result of these preliminary findings, imports of in-scope glass bottles will incur AD cash deposit requirements at rates within the ranges indicated below. As with the countervailing duty (CVD) cash deposit requirements announced in May 2024, AD cash deposits represent payments of estimated tariffs, and any final AD tariff liability will be determined at a later date. The applicable cash deposit rate depends upon the foreign company that manufactured (or exported) the imported bottles, and rates generally vary among manufacturers within each country. The complete list of manufacturers by country and their respective rates can be found at this link.

Key Updates

Preliminary AD and CVD Cash Deposit Rates: The following table shows the ranges of cash deposit rates resulting from Commerce’s recent preliminary AD determinations, along with the CVD cash deposit rates that Commerce announced on May 29, 2024. The AD and CVD cash deposits imposed on imports from China are additive. For example, imports from a Chinese manufacturer with an AD rate of 11.96% and a CVD rate of 21.14% are subject to a combined AD/CVD cash deposit rate of 33.1%.

Effective Date for Cash Deposits: The cash deposit requirements for these duties take effect on August 9, 2024 which is the date the preliminary determinations were published in the Federal Register.

Retroactive charges:

China: Retroactive AD cash deposits apply to imports that entered the US during the 90 days preceding the Federal Register publication date if the glass bottles were produced by Chinese manufacturers that Commerce found to be part of the “China-wide entity.” Imports from manufacturers found to be separate from the China-wide entity do not face retroactive charges.

Mexico and Chile: No retroactive cash deposit requirements apply.

Next Steps

These preliminary findings may change, either because of Commerce’s final AD determinations or the US International Trade Commission’s (ITC) final injury determinations. If both the Commerce and the ITC issue affirmative final rulings, AD and CVD tariffs will be imposed for at least five years.

Here is an updated timeline below. Note that some deadlines have been extended since we provided our original communication.

These decisions introduce a new layer of complexity that producers must consider when sourcing glass for this year and the next.

Bottled Tidbits - Did you know that the standard 750ml wine bottle size was only recently established in the 1970s, to align with global trade and shipping standards?